Higher Taxes Can’t Be the Answer – Part 2

The tax burden includes “excess burdens” few people consider, but which significantly reduce people’s well-being.

In the last essay, we looked a bit at the individual and aggregate tax burdens on individuals, and the costs of tax compliance. In this essay we’ll consider the question: Do the tax laws, and the costs of compliance, at least end up garnering lots of money for the federal government without any adverse consequences that might significantly reduce the benefits of the programs paid for with taxes?

Alas, the answer is no, and at the root of that answer is the separate but very significant cost of tax compliance economists call the “excess burden” of taxes. While taxes are of course necessary to maintain some essential government functions, there are unintended consequences to taxes generally that, while few of us consider them, we all labor (or refrain from laboring) under them.

It’s important to understand exactly how taxes reduce people’s welfare in many ways, even when the taxes aren’t collected. This reduction in welfare is referred to as the “excess burden” of taxes, and to understand what it means Keen and Slemrod offer the example of England’s long-ago tax on windows in houses (which was considered a proxy for wealth), and how the tax led many people to simply avoid paying the tax by reducing the number of windows they had (or by bricking them up so they were no longer windows). As Keen and Slemrod note, “The harm done by vanished windows was not trivial. Poor ventilation spread disease; lack of light led to a deficiency of vitamin B that stunted growth—what the French came to call the ‘British sickness.’” But the concept of the “excess burden” of taxes effects all aspects of what tax policy touches.

While Excess Burden Effects Are Large, They’re Not Intuitive

As Keen and Slemrod write:

The trouble is, that while blocked-up windows make the point obvious, the losses that really matter are almost always manifest in things that cannot be seen, because they are not there: investments not undertaken, for example, or workers not in the workforce. Because they are hard to see and understand, but may well be large, these real costs get too far little attention in tax policy debates … The key lesson is that excess burden is greater the more responsive to taxation is the tax base. The changes in behavior that cause the tax base to change could be real, like blocking up a chimney or deciding not to take on a part-time job, or they could simply be avoidance or evasion, like financing a firm by borrowing rather than injecting new equity, or not declaring the income from a part-time job. In either case, the more responsive the tax base is to the tax rate, the larger is the excess burden per dollar of revenue raised.

As Keen and Slemrod elaborate:

The real burden of taxation does not always fall where it appears, or is intended to … Governments often seem to intend that the impact of a tax fall on some particular group. But taxes do not necessarily stick where they are intended to: Market forces mean that the real burden may be shifted to someone else … Take, for instance, the tax on exports of wool, which from 1275, English kings discovered could raise vast amounts of revenue. The tax was remitted by wool merchants, but landowners like the wool-growing Abbot of Meaux quickly realized that they were the ones who really bore the burden of the tax: “It is those who own the wool who pay this tax to the king, and not the merchants … for wools are sold at a lesser price the greater the tax payable to the king for them.”

And another, more recent example:

In 1990, the U.S. Congress enacted a 10 percent tax on several luxury items, including boats costing more than $100,000, as a compromise measure that would burden the rich without taxing their income at increased rates. But things did not work out like that. The New York Times described the tax as “a stake driven into the heart of [the pleasure boat] industry,” and the Sun-Sentinel reported that “Nationally, yacht sales dipped from 7,500 in 1990 to 3,500 in 1992. There were 30,000 jobs lost nationwide, 8,000 in South Florida, where one in every four of America’s boats is built” … Just because a tax is labeled as being “on” something or someone does not settle its incidence.

Excess burden effects are everywhere:

That taxes generally impose a loss on taxpayers that is greater than the tax actually remitted is made manifest in the examples of tax-induced innovation discussed above. Who would want to live in an unfinished house, or one with a tiny door, if it were not to save taxes? These are all what are called “distortions”: things that are done only because of incentives created by the tax system. And their importance is that they create a loss from taxation over and above that which the private sector must inevitably suffer from transferring resources to the government. The idea of this additional loss from taxation—“excess burden”—is one of the most fundamental and powerful of all ideas that can be brought to bear in thinking about taxation, yet it is rarely picked up in public debate. Perhaps it seems nerdy. But it is not as mysterious as it may seem. And it matters … The trouble is that [excess burden] is very nebulous. It does not show up in anyone’s budget. And it usually takes the form of things that are not there ([like] the profits and wages not earned because of an investment that did not happen) or actions that are not taken (the overtime not worked or the entrepreneurial career path not chosen).

When one sees how tax policy effects people in this way, the import of Joseph Schumpeter’s statement becomes more clear: “The spirit of a people, its cultural level, its social structure, the deeds its policy may prepare— all this and more is written in its fiscal history, stripped of all phrases.”

Measuring the Excess Burden of Taxation

The excess burden effect has been around since taxes themselves, with evidence for it recently being mined from events almost 300 years ago. As Keen and Slemrod write:

The English tax on hearths was replaced by the tax on windows, also an indicator of how opulent a house is but one that could be measured in a less intrusive way. We mentioned that one response of English homeowners was to brick up some windows. In 1848, the president of the Carpenters’ Society in London testified to Parliament that almost every house on Compton Street in Soho had employed him to reduce the number of windows. One feature of the window tax was that liability jumped once a certain number of windows was reached—what we earlier called “notches.” Centuries later, such notches have turned out to provide a clever way of gauging the extent of excess burden. To see how, go back to 1747. No tax was then paid on properties with fewer than 10 windows, but for those with between 10 and 14, a tax of 6d was payable on each and every window—not just the number exceeding that threshold. An inspired study applies this insight to local window tax records for 493 English homes, mostly from the town of Ludlow in Shropshire, between 1747 and 1757. Sure enough, these records show a massive spike in the number of houses having exactly nine windows: more than four times as many as had either eight or 10. And there were similar spikes at 14 and 19 windows, reflecting further notches in tax liability at 15 and 20 windows. There was simply far too much bunching to be attributable to just chance. Given the kind of responsiveness that could explain this pattern, the implied excess burden of the tax is estimated, for the average property, to be about 13 percent of the revenue raised by the tax. However, for those who wound up cutting back to exactly one of the notches—to 14, for example—the excess burden was much larger, at about 62 percent of the tax payable. Among these, for those who cut to nine windows, and so had no liability, the tax was pure excess burden: no revenue was raised from them, but their behavior was distorted.

Regarding more recent evidence:

The decision of whether or not to work at all … proves quite responsive to taxation, over and above this inevitable effect (particularly among women), and so the excess burden per dollar raised from taxes that discourage labor force participation can be pretty large … For the income tax, reams of articles have tried to estimate the “elasticity of taxable income.” One recent survey of this vast literature settles on a typical elasticity of taxable income between 0.2 and 0.3. Here’s what that means. Say the income tax rate increases from 30 percent to 37 percent. Then the “net-of-tax rate” (the percentage of a dollar earned that the earner gets to keep) falls from 70 percent to 63 percent, a 10 percent decline. An elasticity of taxable income equal to between 0.2 and 0.3 suggests that reported taxable income would, in response to the tax increase, fall between 2 percent and 3 percent.

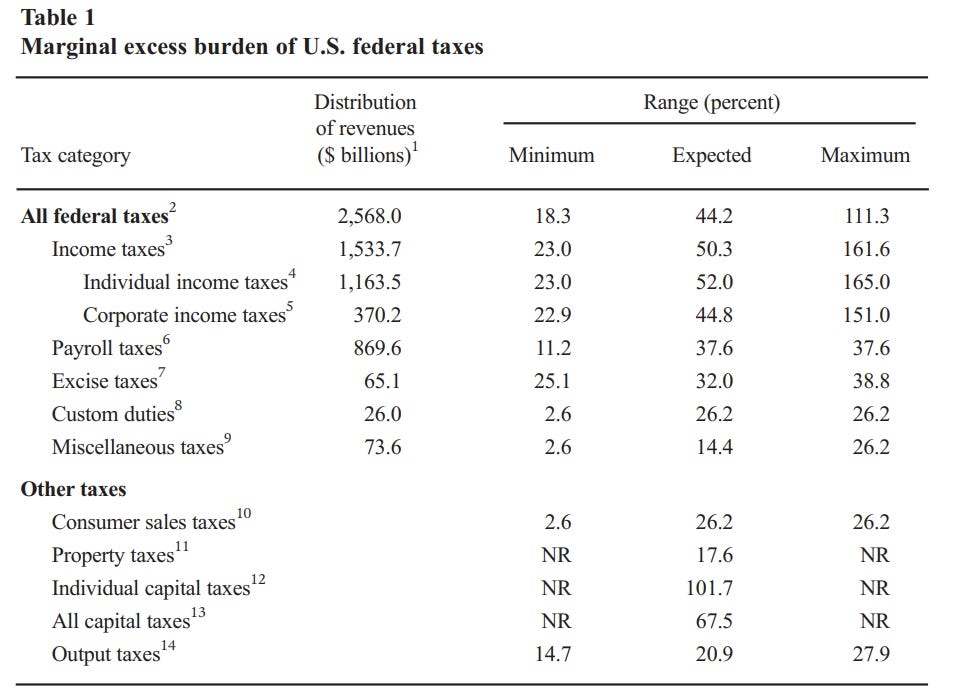

A paper from the CATO Institute further compiles how economists have measured excess burdens. One survey of the relevant literature found that “Estimates vary depending on the type of tax, but the “marginal excess burden” of federal taxes most likely ranges from 14 to 52 cents per dollar of tax revenue, averaging about 44 cents for all federal taxes.”

As the CATO Institute paper points out, “For nearly two decades, the U.S. Office of Management and Budget has directed federal agencies to include an average marginal excess burden of 25 cents per dollar when conducting cost-benefit analyses of federal programs.”

All this means that

Economists have confirmed empirically what most laymen understand intuitively: “whatever you tax, you get less of.” Taxes on labor, such as income and payroll taxes, tend to reduce the amount people will work. Consumption taxes, like sales, excise, and value-added taxes, reduce the consumption of the taxed items. Capital taxes, such as those on property, dividends, or capital gains, decrease the desirability of investing and reduce the amount of savings available for capital investment. All of these predictable changes in human behavior reduce output (present or future) in some form, thereby reducing the economic welfare of consumers, producers, or both.

As Keen and Slemrod ask:

What would the founding fathers of the income tax—Pitt, Addington, Taft, Caillaux, and the others—make of their creation if they were to see it today? … [They would] be dumbfounded by the massive increase in the size of government to which the income tax has contributed: exactly the monster that many of them and their contemporaries had dreaded they were unleashing. And the progressive structures we now take for granted might seem to Gladstone, for one, as obvious validation of his fear that graduation would mean a “direct tendency to communism.” The high marginal tax rates—an average top statutory personal income tax rate of 43 percent in the OECD in 2019—would leave them puzzled that industry and endeavor had not entirely dried up.

What to do about the problem of excess burden? As Keen and Slemrod write:

[T]he basic prescription for limiting excess burden (but not wholly eliminating it) is to interfere as little as possible with the choices that businesses and people make as to how to go about doing the things they do—unless there is good reason to do so. The reasons are somewhat different in the two cases. Interfering with businesses’ input decisions tends to reduce the total output produced from available resources, which is very unlikely to be a good thing … [B]eyond a few broad ideas—notably the implication of the principle that goods with especially inelastic demand are attractive targets for high taxation on efficiency grounds—we know little about how best to do this in practice. All kinds of differentiation, in any case, open the door to lobbies and special pleading.

These negative results of taxation also can’t be avoided by deciding “where the legal liability for remitting a tax lies, meaning who writes the check to the government.” As Keen and Stemson explain:

The Emperor Nero at one point ordered that the 4 percent sales tax on slaves be remitted by the seller instead of the buyer. The Roman historian Tacitus, however, realized that “the tax of one twenty-fifth part of the goods for sale was remitted, nominally rather than with any real effect, because although the seller was ordered to pay it, it accrued to the buyer as part of the price.” In effect, Tacitus noted that the identity of the remitter mattered not at all.

So we really can’t avoid these profoundly negative “excess burden” results of taxes. So best to keep taxes low. Edmund Burke, the 18th century English statesman, wrote of the danger when government officials with limited knowledge try to implement one policy regarding a certain group of people without knowing the effects of those policies on many other people:

An ignorant man, who is not fool enough to meddle with his clock, is however sufficiently confident to think he can safely take to pieces, and put together at his pleasure, a moral machine of another guise, importance and complexity, composed of far other wheels, and springs, and balances, and counteracting and co-operating powers.

Links to all essays in this series: Part 1; Part 2; Part 3; Part 4; Part 5; Part 6; Part 7; Part 8