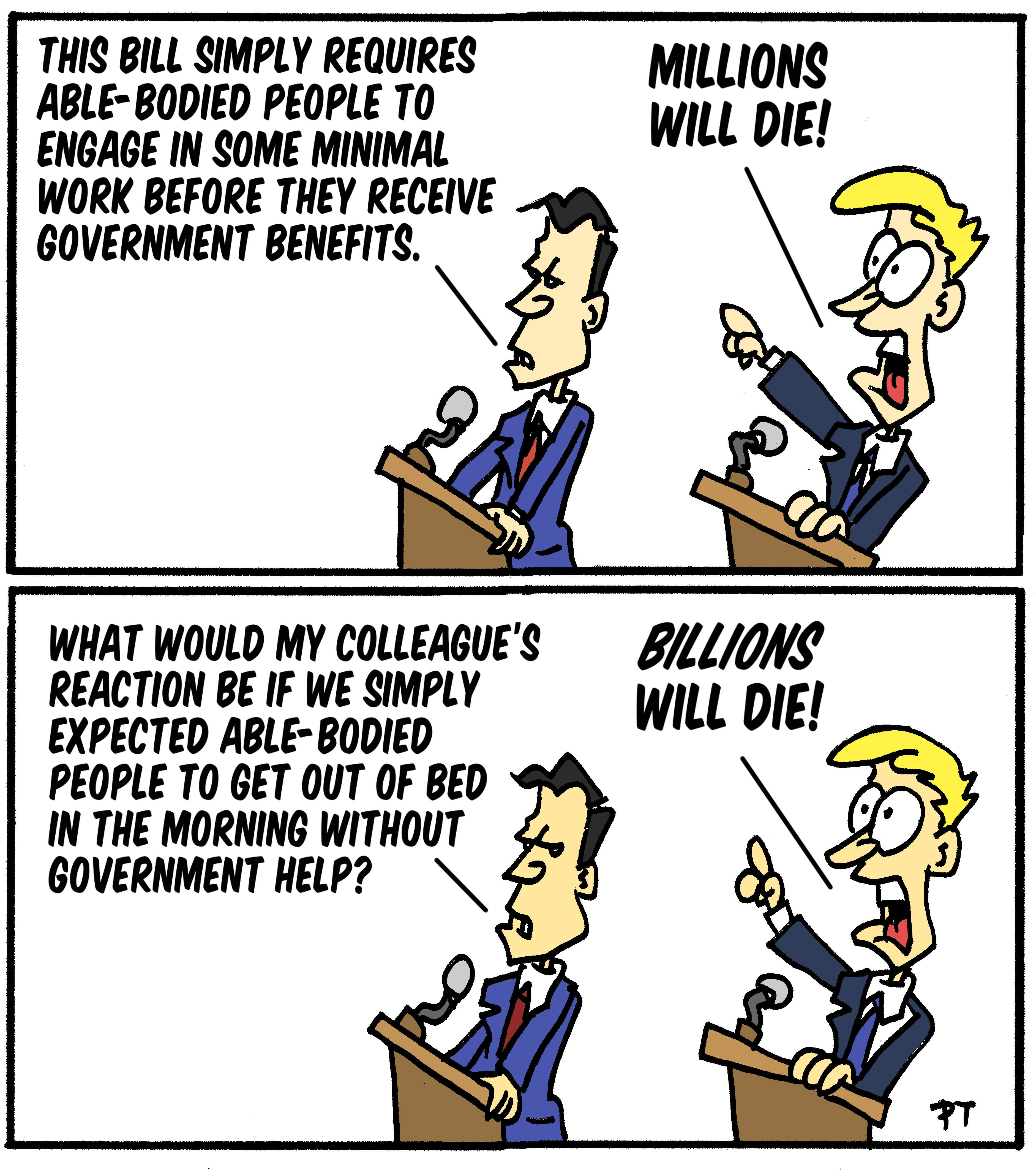

“MILLIONS WILL DIE!”

But only if they just sit there.

In a previous essay I explored some reasons why government is only legitimate, and sustainable, if it provides no more than a minimal social safety net reserved solely for those who don’t have any physical or financial means of doing things for themselves. In this essay, I’ll explore a common rhetorical response by those who support an ever-increasing welfare state: namely, “Millions will die!”

A bill was recently enacted into law that makes the following changes to federal benefits programs.

Regarding Medicaid, the One Bill Beautiful Bill imposes work requirements for able-bodied adults in Medicaid expansion states: about 80 hours of work a month. The Congressional Budget Office projects that over 10 million people will lose Medicaid coverage over the next decade because they will choose not to comply with these requirements.

Regarding federal food assistance programs, the new law implements stricter work requirements for SNAP recipients who are not disabled, and who do not have children. The CBO projects that about 3.2 million people will lose federal food assistance benefits over the next ten years because they don’t meet those requirements.

I suspect that if most people realized these benefits cuts are based on reasonable coverage criteria that reserve scarce taxpayer dollars for those whose circumstances more clearly justify those benefits, there would be more support for the legislation than there already is. But many people won’t get past the refrain of opponents of those reforms, such as House minority leader Hakeem Jeffries who said “People will literally die” as a result of those work requirements, and the Center for American Progress, which claims deaths resulting from those work requirements will number in the “tens of thousands of Americans each year.”

Of course, all those predictions of increased deaths assume without evidence that the people who choose not to meet these new requirements, or don’t meet the new requirements, will do nothing within their power to obtain the same or similar benefits through other means that would allow them to pay for those benefits themselves. After all, most people don’t want to die and will adjust their behavior to prevent that from happening. As Hollman Jenkins Jr. writes in the Wall Street Journal, “When a program goes away, after all, people may adapt and find new solutions for themselves. They may choose not to die.”

Betting on the preference not to die, which after all is the central premise of evolution, would seem to be a pretty safe bet. And we have past evidence that people will adapt to survive in such circumstances. As Phil Gramm, Robert Ekelund, and John Early write in their book The Myth of American Inequality: How Government Biases Policy Debate:

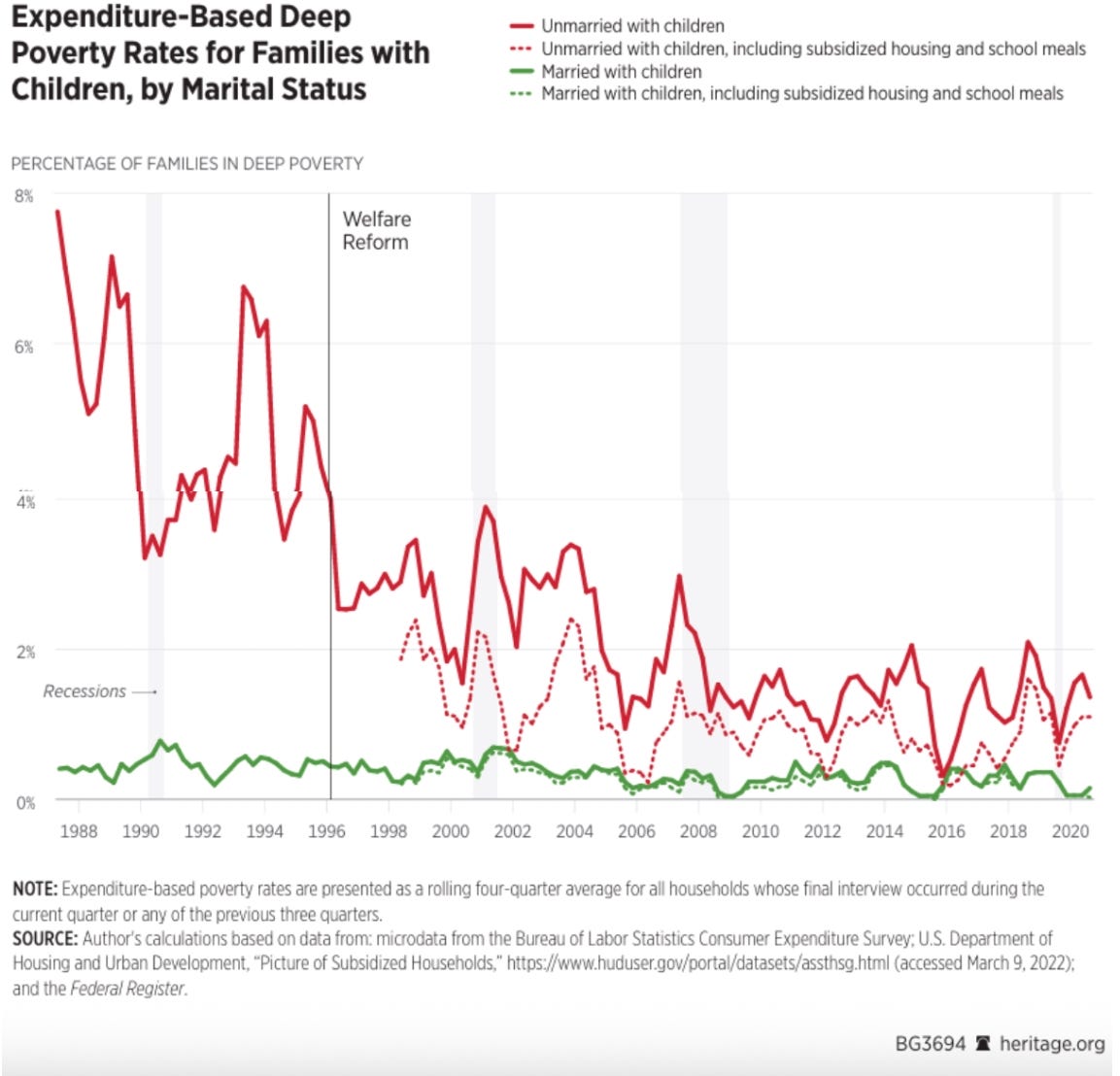

There has been only one significant attempt to reverse this fifty-year trend of reduced work and increasing dependency. The Personal Responsibility and Work Opportunity Reconciliation Act of 1996 (P.L. 104-193), or simply the Welfare Reform of 1996, was a bipartisan effort by President Bill Clinton and a Republican Congress. It replaced the Aid to Families with Dependent Children transfer payments with the Temporary Assistance for Needy Families. Both the old and the new programs served only households with children, about 90 percent of which were headed by a single mother. The welfare reform endeavored to wean these families off welfare and build their self-reliance by creating stronger requirements for work or training. It also set more stringent time limits on receiving aid. The 1996 reforms were successful. The number of families receiving payments declined by more than half. Much of the decline was the result of beneficiaries finding employment. As a result, employment among low-income single parents rose. Poverty for single-mother families declined and has continued to remain lower than it was before the reforms. Single-mother poverty also declined relative to poverty for other types of families and has remained lower ever since.

Indeed, the liberal Brookings Institution found at the time that the work requirements in the bill President Clinton signed into law incentivized people to get jobs such that, ten years later, people were better off than they were before the reforms.

As Matt Weidinger writes of the work requirements in the more recent legislation:

[T]he new law also is noteworthy for leaning on key welfare reforms with a proven track record of success. Those policies—namely, applying work requirements and creating a financial interest for states to limit benefit rolls—achieve significant benefit savings now and should be expanded in the future to further boost work and keep federal deficits in check … Several of the biggest savers reprise past policies designed to tame welfare benefits. First, the [legislation] expands work requirements for able-bodied adults receiving Medicaid and food stamps. As Trump administration officials noted in a New York Times opinion, work requirements are widely supported and were a signature feature of the bipartisan welfare reforms Bill Clinton signed in 1996. That historic law ended a New Deal-era program that entitled nonworking parents to limitless welfare checks and replaced it with the Temporary Assistance for Needy Families (TANF) program, which expects adults to work or train as a condition of eligibility. The results were remarkable, with more parents going to work, poverty falling, and caseloads ultimately plummeting 85 percent … The [legislation] also strengthens the work requirement for able-bodied food stamp recipients, adding another $70 billion in savings. These reforms can and should be expanded to expect recipients of public housing and other benefits to similarly prepare for work instead of perpetually depending on taxpayer aid. Driving these large savings is a simple fact: for able-bodied adults, federal taxpayers today support all food stamp and most Medicaid costs. Those federal commitments are open-ended, so states often welcome bigger caseloads that confer more federal funds. That dependency-inducing dynamic has contributed to soaring food stamp and Medicaid caseloads, especially in blue states. It also contrasts sharply with the TANF program, whose fixed federal block grant (which hasn’t been adjusted even for inflation since 1996) and required state match promote smaller caseloads and less spending. Since the mid-1990s, the number of households on food stamps has grown from twice to now over 20 times the number on TANF.

As Matt Weidinger explains, the reduction in dependency we can expect from these added work requirements will largely just amount to bringing dependency levels back to pre-COVID rates:

Welfare expanded rapidly during the pandemic, and significant caseload expansions have continued even after it ended. Medicaid and the Children’s Health Insurance Program exploded from a pre-pandemic 71 million recipients to 94 million in March 2023, when pandemic-driven policy expansions started to unwind. While down, current caseloads remain over 78 million, still 10 percent above pre-pandemic levels. Food stamp caseloads similarly spiked, rising sharply from 37 million to over 43 million in the first months of the pandemic. Today’s caseload remains just off that peak and still 14 percent above the pre-pandemic level. New reforms are projected to notably reduce both Medicaid and food stamp caseloads, returning them closer to pre-pandemic levels. The biggest reductions are projected to result from expanded work requirements included in Republicans’ One Big Beautiful Bill (OBBB). Work requirements are widely supported by the public and contributed to remarkable results in the past. For example, Republican welfare reforms signed into law by Bill Clinton featured work requirements for welfare checks that contributed to more parents working, poverty falling, and cash welfare caseloads plummeting 85 percent. The OBBB dusts off that playbook by applying similar “community engagement requirements” to able-bodied adults on Medicaid, expecting them to perform 80 hours of work, education, or community service in at least two months per year. Nondisabled childless adults on Medicaid spend an average of 125 hours per month watching TV or playing video games, so most should have ample time. The Congressional Budget Office estimates this part-time, part-year requirement will save taxpayers $325 billion over the next decade while removing 4.8 million able-bodied adults from the Medicaid rolls. The new law similarly strengthens work requirements for food stamps, saving another $70 billion while reducing that caseload by three million able-bodied adults. Other recent changes focus on specific groups, such as the Trump administration’s July 10 regulations ending illegal alien access to Head Start and postsecondary education subsidies. Additional changes in the OBBB will end child tax credit payments to households headed solely by illegal aliens.

As Kevin Corinth writes, work requirements also help the children of recipients of government aid by increasing the resources available to families:

There is indeed a substantial body of evidence that more income is good for kids—it can improve their academic performance in the short run and their outcomes as adults in the long run. But there is an important caveat: Whether there are strings attached to the income makes a difference. Income assistance that requires work, in the form of the Earned Income Tax Credit (EITC), has shown the strongest evidence of boosting kids’ development. The evidence for support not tied to work is generally weaker or relies on evidence from over half a century ago through the rollout of Food Stamps and other programs when baseline material wellbeing was far lower. The importance of conditioning assistance on work has previously been recognized. In a widely cited 2016 volume for the National Bureau of Economic Research, Austin Nichols and Jesse Rothstein conclude, “there is robust evidence of quite large effects of the EITC on children’s academic achievement and attainment,” compared to “relatively small estimates of effects of family income on student outcomes that come from non-EITC settings.” Likewise, a 2014 article published in the Quarterly Journal of Economics posits that housing assistance does little to improve child outcomes compared to the EITC because the EITC promotes work …

Remember that all the Congressional Budget Office predicted was how many people might lose their federal benefits under new work requirements, not how many people would die as a result of those requirements. When CBO projects that in 2034, 11.8 million fewer people will have health coverage because of the new Medicaid rules, that doesn’t mean those people won’t make decisions and take actions that get them health insurance coverage elsewhere.

The ”Millions will die!” absurdity is not only based on the assumption that people will not take minimal efforts to save their own lives, but it implicitly posits that any government action or inaction that incentivizes personal responsibility will result in people dying because people will refuse to do things for themselves if the government won’t do those things for them. As Hollman Jenkins Jr. writes, “Sen. Elizabeth Warren (D., Mass.) has been a fiery proponent of ‘people will die’ opposition to spending cuts. But people will die no less from Ms. Warren’s failure to push through new programs or expand existing benefits to new classes of Americans.”

Studies have shown that when the IRS mailed letters to uninsured individuals simply pointing out that they could apply for coverage, more people signed up for and received the health insurance. As the researchers report:

We evaluate a randomized pilot study in which the IRS sent informational letters to 3.9 million taxpayers who paid a tax penalty for lacking health insurance coverage under the Affordable Care Act. Drawing on administrative data, we study the effect of the intervention on taxpayers’ subsequent health insurance enrollment and mortality. We find the intervention led to increased coverage in the two years following treatment and that this additional coverage reduced mortality among middle-aged adults over the same time period.

So when people are reminded they can do something on their own, more people do things on their own. Under the “millions will die” understanding, then, deaths result every day the federal government fails to remind people of a whole bunch of things they could do to help themselves. Indeed, perhaps “millions will die” because people come to believe the false “millions will die” rhetoric and incorrectly assume they can’t do anything to provide health insurance for themselves. Clearly, there comes a point at which people simply have to be expected to exercise their capacity to help themselves, or they will exercise that capacity less and less.

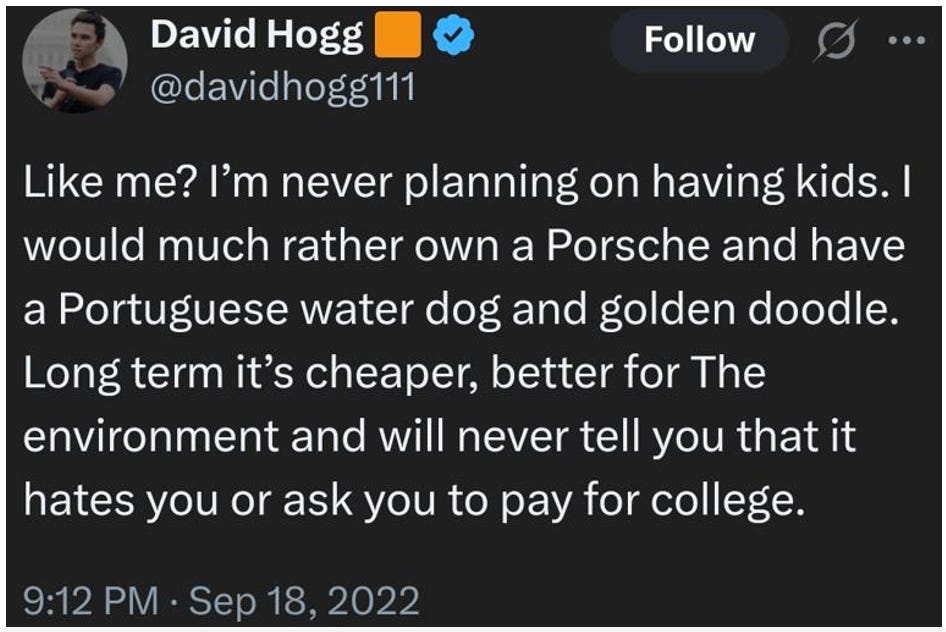

People act on false or dramatically exaggerated claims all the time, and always will. For example, people who believe the false or dramatically exaggerated predictions of the dire consequences of climate change, such as former Vice Chair of the Democratic National Committee, David Hogg, are even choosing to never have kids as a result.

Of course, fewer children today will inevitably lead to fewer working adults tomorrow, while there will be more and more non-working seniors relying on government benefits, which can only make all government welfare programs less fiscally sustainable in the future -- in which case the familiar false logic leads to David Hogg himself helping cause “Millions to die!”

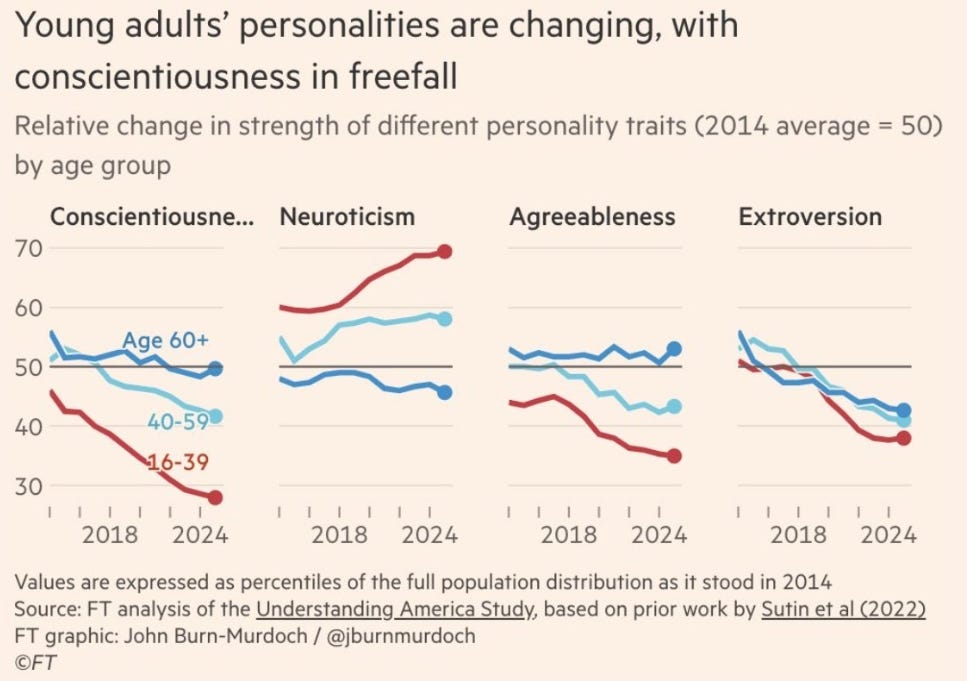

And Hogg relayed his message over smartphones and social media, which, as entertainment crutches, are likely contributing to the significant decrease in self-reliance reported among young people today. The Financial Times published an analysis of American personality changes using data from the Understanding America Study. Over a decade, conscientiousness — the trait most closely linked to responsibility, follow-through, and self-control — dropped among young adults. Older adults remain essentially unchanged, suggesting the use of smartphones for entertainment may be at play here.

American law doesn’t allow people to sue Congress for negligently drafting legislation, but if it did, should Congress be considered legally responsible for causing harm by adding work requirements to the receipt of welfare benefits? Lawyers who think about the “Millions will die!” line of argument may be reminded of some relevant common-sense legal concepts, like “but for” and “proximate” cause.

Black’s Law Dictionary defines “but for” cause as “The cause without which the event could not have occurred.” In Comcast v. National Association of African American-Owned Media, the Supreme Court stated that “Few legal principles are better established than the rule requiring a plaintiff to establish causation [of injury]” and that “In the law of torts, this usually means a plaintiff must first plead and then prove that its injury would not have occurred ‘but for’ the defendant’s unlawful conduct.” Of course, in the case of “Millions will die!” there are several “but for” causes that may be relevant. For example, someone might die because of an ailment they didn’t have treated when it would have been treated “but for” the lack of health insurance. But such person might also have gotten health insurance “but for” their failure to fulfill the minimal work requirements attached to a health insurance benefit. Because there can be multiple “but for” causes for any particular bad result, American law has added another concept called “proximate cause” that must be found before liability for harm can result.

Black’s Law Dictionary defines “proximate cause” as “A cause that is legally sufficient to result in liability; an act or omission that is considered in law to result in a consequence, so that liability can be imposed on the actor.” To succeed with a personal injury claim based on negligence, one has to show both “but for” and “proximate” causation. But proximate cause is a policy matter. As the authors of a leading legal treatise write, “As a practical matter, legal responsibility must be limited to those causes which are so closely connected with the result and of such significance that the law is justified in imposing liability. Some boundary must be set to liability for the consequences of any act, upon the basis of some social idea of justice or policy.”

One such policy that has developed in the law, and which should be applied more generally to government policy, is that of putting responsibility for something on “the least cost avoider,” including individual people who are capable of helping themselves, and as such can avoid injury to themselves.

What’s a “least cost avoider?” As Ward Farnsworth describes the concept of the least cost avoider in The Legal Analyst: A Toolkit for Thinking about the Law:

[W]hen there’s an expense, just send the bill to whoever could have avoided it most cheaply, either by taking precautions or by switching to some activity less likely to create such expenses. The expenses might arise from an accident, or a misunderstanding, or an agreement that fell through. All those events can be costly, and all might be handled the same way: figure out who was in the best position to prevent it—we will call this person the least (or cheapest) cost avoider—and make him pay for the result. Sometimes we might hope he will act differently next time, but not necessarily; the point might be just to force him to compare the cost of paying the bills with the cost of taking more precautions, and do whichever is cheaper. The beauty of this approach is that the law doesn’t have to figure out how a single owner would have handled the problem. It tells the least cost avoider to figure it out. Maybe he will decide to let the bad things happen and keep paying the bills, or maybe he will find less expensive ways to prevent them. In either case he will feel the full cost of his decisions and so will make them carefully.

As Farnsworth writes, “one of the great advantages of throwing legal responsibility for harm onto whoever can avoid the harm most cheaply” is that “It’s easy” because “[all] you might need to know [is] what precautions each party could have taken, how much trouble the precautions would have been, and how much they would have reduced the chances of the disaster.”

For example:

Liability for blasting [with dynamite] is strict, but that doesn’t mean it’s absolute; the blaster can still get off the hook in certain cases, as when the injured plaintiff assumed the risk of injury. Perhaps he knowingly drew near to the dynamiting operation out of irrepressible curiosity. One way to think of such a case is that the victim then became the least cost avoider after all. He knew what he was getting into and should have stayed away. That is why the law makes an exception here to the usual rule that holds the blaster liable. This business of the victim’s own role in the accident is important … Throwing all the liability onto the least cost avoider of some bad thing tends to make sense when there is just one party whose behavior we want the law to influence, usually because that one party has all the control over whether the bad thing happens … [T]he least cost avoider is the person who can avoid the disaster most easily, where “easily” is read to include not only the power to take precautions but the power to foresee the need for them, figure out what the options are … The general idea of placing liability on the least cost avoider is powerful and makes a lot of legal problems easier to understand. To stay with tort law for a moment, think of cases where one person is sued for failing to rescue another who was drowning. The usual rule is that the defendant wins; there is no duty to rescue strangers from trouble. Again, one way to think about the rule is that the victim is usually the least cost avoider of the disaster; it’s easier for victims to avoid getting themselves into trouble than it is for rescuers to get them out of it. So in effect the victim is held liable for his own fix, which is to say that he can’t sue anyone else who might have helped him afterwards but didn’t.

And so it is with people who decide not to satisfy minimal work requirements to obtain health insurance: they are the least cost avoiders. The government, with all its cumbersome and expensive ways of doing things, need not always come to the rescue when people can help themselves.

To get more technical, federal judge Learned Hand came up for a basic mathematical formula for determining who was the least cost avoider in a given situation. In the interesting 1947 case of U.S. v. Carroll Towing Company, the mooring lines of the ship The Anna C were loosened or came undone, causing the barge to drift away from the pier and strike a tanker, which lost its cargo. There was no one on board the barge at the time of the incident, and the question was whether the barge owner was liable for the accident. In his opinion, Judge Hand wrote:

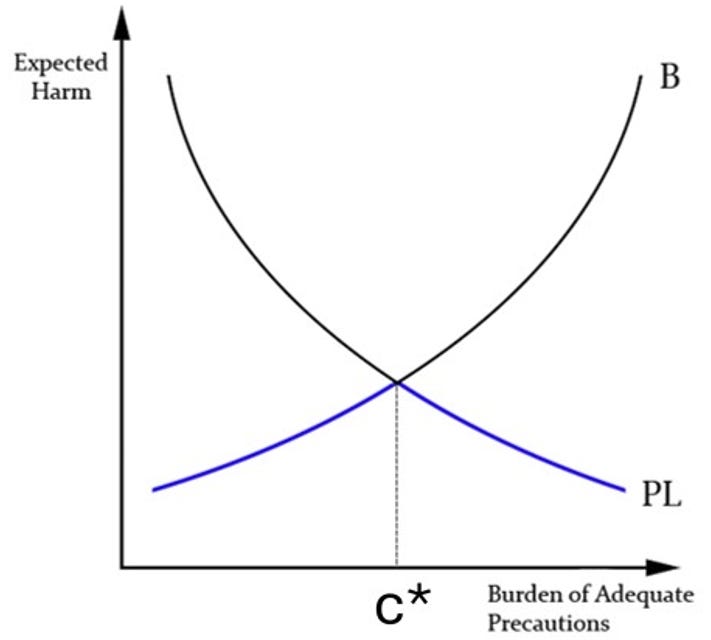

[T]he owner’s duty, as in other similar situations, to provide against resulting injuries is a function of three variables: (1) The probability that she [the ship] will break away; (2) the gravity of the resulting injury, if she does; (3) the burden of adequate precautions. Possibly it serves to bring this notion into relief to state it in algebraic terms: if the probability be called P; the injury, L; and the burden, B; liability depends upon whether B is less than L multiplied by P: i.e., whether B less than PL.

As Richard Posner writes in An Economic Analysis of Law (Fifth ed. 1998):

The Hand Formula in its correct marginal form is presented graphically in Figure 6.1 [below]. The horizontal axis represents units of care, the vertical axis (as usual) dollars. The curve marked PL depicts the marginal change in expected accident costs as a function of care and is shown declining on the assumption that care has a diminishing effect in preventing accidents. The curve marked B is the marginal cost of care and is shown rising on the assumption that inputs of care are scarce and therefore their price rises as more and more are bought. The intersection of the two curves, c*, represents due care … To the left of c* the injurer is negligent; B is smaller than PL. To the right, where the costs of care are greater than the benefits in reducing expected accident costs, the injurer is not negligent …

So where the burden of adequate precaution (B) is low (like having to comply with some minimal work requirements to get health care coverage) and the probability of loss (PL) for failing to do so is high (like where failing to comply with minimal work requirements may leave one without any health insurance at all), someone who fails to comply with the work requirements is going to be considered the least cost avoider.

Hand’s Formula also provides a good template for public policy. As Stephen Gilles writes:

A cheapest cost-avoider rule requires the court (or legislature) to make a general judgment concerning the cheapest means of avoiding a particular category of accident risks (and the person identified with those precautions). An optimal care rule requires the court (or legislature) to make a general judgment concerning the optimal level of care with regard to some identifiable category of accident risks -- that is, to decide whether the cheapest means of avoiding those risks should in fact be employed … [T]he better-and more general-formulation of the cheapest cost-avoider criterion simply asks which party could, at lowest overall cost, have avoided the accident.

Government largess in the delivery of welfare benefits, of course, also leads to fraud and the provision of services people don’t end up using. As the Wall Street Journal writes:

[T]he Paragon Institute reports that taxpayers are subsidizing insurance for nearly 12 million people who never use their coverage … Democrats in 2021 sweetened subsidies for buying insurance on the ObamaCare exchanges. Enrollment has since doubled while taxpayer costs rose by 150%. Spending on ObamaCare subsidies has increased faster than Medicaid or Medicare since 2020, if you can believe it. Democrats tout this blowout of government-subsidized healthcare as a triumph. Here’s the wild part: More than a third of all enrollees generated no medical claims last year, according to Paragon’s analysis. That includes 40% of those in plans that are fully subsidized. Between 2021 and 2024, the number of enrollees who didn’t use their health coverage more than tripled to 11.7 million from 3.5 million. As Paragon explains, tens of billions of dollars in subsidies for these 11.7 million enrollees “went to insurers and middlemen without funding a single medical service.” … Paragon estimates that about 6.4 million people this year were improperly enrolled in exchange plans. The Justice Department has charged several brokers with enrolling consumers in ObamaCare plans for which they weren’t eligible in order to obtain commissions. This is why Republicans in their tax bill strengthened income verifications for ObamaCare plans. Democrats claim such measures will cause millions of people to lose coverage. But many of them don’t need or use their insurance. Some are enrolled in employer plans or Medicaid. The subsidies pad the profits of insurers.

Further, and perversely, expanding government benefits often leads not to less initiative on the part of benefit recipients, but to increased initiative in figuring out ways to maximize their receipt of government benefits. Some interesting historical perspective is provided in a 1940 book titled The Unemployed Worker: A Study of the Task of Making a Living Without a Job, by economist E. Wight Bakke at the Institute of Human Relations at Yale University. The book is based on surveys of unemployed workers during the Great Depression “undertaken for the purpose of discovering the readjustment problems faced by unemployed American workers and their families.”

Bakke writes:

When one's income from wages becomes insufficient for maintenance of habitual standard of living, one may call on additional resources not strictly the result of independent effort in the following order of the departure from the normal circumstances of self-support:

1. Accrued benefit rights [that is, pension benefits, accumulated vacation time, or other benefits that accumulate under employment contracts as an individual continues their employment].

2. Commercial credit.

3. Savings of others than head of the family.

4. New working members of family not normally expected to earn.

5. Borrowing on property.

6. Clan aid -- loans to gifts.

7. Friends loans to gifts.

8. Government work relief.

9. Associations in which individual has membership.

10. Community assistance cash to commodity.

Note that, at the time, “government work relief” is very low on the list. As Bakke writes in a subsection titled “The Attempt to Keep Off Relief”:

In 1933 a sample study involving 2,000 representative New Haven families revealed 988 individuals to be unemployed. In 1935, two years later, these 988 were revisited to learn how many had sought relief. Less than one fourth (24%) had done so, the majority of these asking for only partial support. Half of this 24% had had contacts with relief agencies prior to this period of unemployment. How long did the other half wait after the layoff before crossing the threshold of the relief office for the first time? Ten per cent applied in less than three months, 17% in less than six months, 30% in less than one year after unemployment. Even after two years of unemployment 40% of this applying-for-the-first-time group were "getting by" somehow without public assistance … These facts, although they give no explanation of the refusal of men to apply for public assistance, do indicate a combination of resources, resourcefulness, and tenacity in holding to social standards of independence over considerable periods during which normal income was greatly reduced or completely lacking.

Bakke continues:

One fact … cannot be denied. Those who had no personal contact with such [government relief] agencies wished to steer clear of them. Such phrases as "rather be dead and buried," "would hide my face in the ground and pound the earth" were common … The struggles to maintain independence recorded in our case histories are a vivid reminder that the fight was no sham battle for the sake of appearances, but an honest struggle into which went every device and power at the disposal of the worker and his family … [And] [t]he socially “proper” thing for a relief client is to get off relief as quickly as possible and back into private employment.

But interestingly, Bakke also explores the sort of inverse “self-reliance” that tended to develop over time among those who took government relief, namely ingenuity in “milking the system.” As Bakke writes:

The evidences are too clear for any observer to miss that "self-reliance" is not dead, that relief clients do study and learn the techniques by which to increase the level of their subsistence in the way indicated by their accusers. An investigator for the D.P.C. [Department of Public Charities] reported some interesting experiences in this connection. She is Italian but is light-skinned and fair-haired and decidedly un-Italian looking. Her main work has been the investigation of Italian families on the F.E.R.A. [Federal Emergency Relief Administration]. The fact that she did not look Italian has caused her to overhear conversations in Italian, indicating the attitude of the clients toward relief. For example, while sitting in the front room talking to the wife, the wife will call out to a child to come and see the investigator, but she will warn the child to put on his old shoes first. Or she will hear the mother or father tell someone in the back of the house to put away the wine or the food before the investigator comes into the house. Her method is not to tell them she knows Italian but to cut the budget in accordance with the conversations she has overheard. Her opinion is that you have to be hard-boiled and ruthless in dealing with the people on relief or they will "run away with the place." … Most social workers could tell stories about clients who were able to withhold information about their resources … Mr. Crandall learned that the D.P.C. often will pay rent if the landlord evicts the family. Therefore, he and his landlord made it up together that he was to send Mr. Crandall eviction papers. In return Mr. Crandall agreed to pay him the $10 which the D.P.C. is supposed to pay when eviction papers are given. They hope that the D.P.C. will continue to pay the $10 a month. The landlord has promised to paper the kitchen for them if they get this money … [Another] observer asked, "It doesn't pay to give them a straight story, does it?" "Oh, Christ! You'll never get anything if you tell the truth. You gotta be wise, give them a good story." Such evidences of what nonrelief citizens call "chiseling" are as good examples of initiative in learning the techniques of increasing the security from relief … [Another relief recipient noted] “There was [a] family downstairs and they always seemed to have nice clothes even though they were getting a charity order and not working at all. Then reading the papers I found out we could get more, so what did I do? I called up the Charities Department and told them that if we didn't get some milk and other things we were going to steal them. I kept the kids home from school two days and called up the principal and told him the kids weren't coming to school until they had clothes enough to keep them warm. The next day the social worker came up and they sent clothes and blankets and shoes so that they covered the whole floor here. It was more than we needed. Then the city gave us a $3 order and sent milk … If I had known all along what I found out the last year, we could have been living wonderful for the last four years. What you got to do is use up what you got and make a big holler for more. Then they give you what you ought to have.”

Regarding a relatively rare counterexample, Bakke recounts that

The investigator who came to the Curleys was amazed at the cheap rent which they had. Mrs. Curley was pleased. She said she told the investigator that she was able to manage on the $12 a week even though she had a very large family. But the way she managed was to be content to live in a cheap rent and to walk around from store to store to find the cheapest food. She said the investigator thought she was very clever, and told her that many people wanted more money, but few were willing to walk around and try to manage on what they did have.

As Bakke summarizes his thoughts on the issue:

"Practice makes perfect." We have seen that relief recipients are inevitably stimulated to learn and practice the techniques of "getting all they can." Concentration on such an endeavor assumes a larger proportion of their conscious efforts. Men become what they practice. If the source of self-maintenance is a relief agency they become persons who try to get the maximum in satisfaction of their needs from that agency. In the absence of other sources, this effort dominates their attention and becomes necessarily their chief interest. The longer they are on relief, the more practice they get. The more agencies they visit, the greater variety of techniques they are forced to learn. The more the giving of relief depends upon making out a bad picture of their situation and their own helplessness, the more they will "talk poor mouth" to use an old New England phrase.

Perhaps “Millions will die!” is the new “talk poor mouth” among many in the modern political class.

Paul, Great piece. Perhaps even Trillions will die if we wait long enough. I wish everyone had to read this. I will spread to anyone who might. Thanks for doing this.